The CEVA Almajdouie Saudi logistics merger story, structured as a joint venture, sits inside a market that is growing and also reorganizing. In October 2024, CEVA Logistics and Almajdouie finalized an agreement to form CEVA Almajdouie Logistics, combining both companies’ transport and logistics operations to deliver end-to-end integrated supply chain services across Saudi Arabia. Another industry account describes the same 2024 move as a joint venture that consolidates their respective transportation and logistics operations in the Kingdom by combining Almajdouie’s domestic infrastructure with CEVA’s international network. The message is practical: customers increasingly want one provider that can link industrial hubs, freight, warehousing, and distribution through a single operating model.

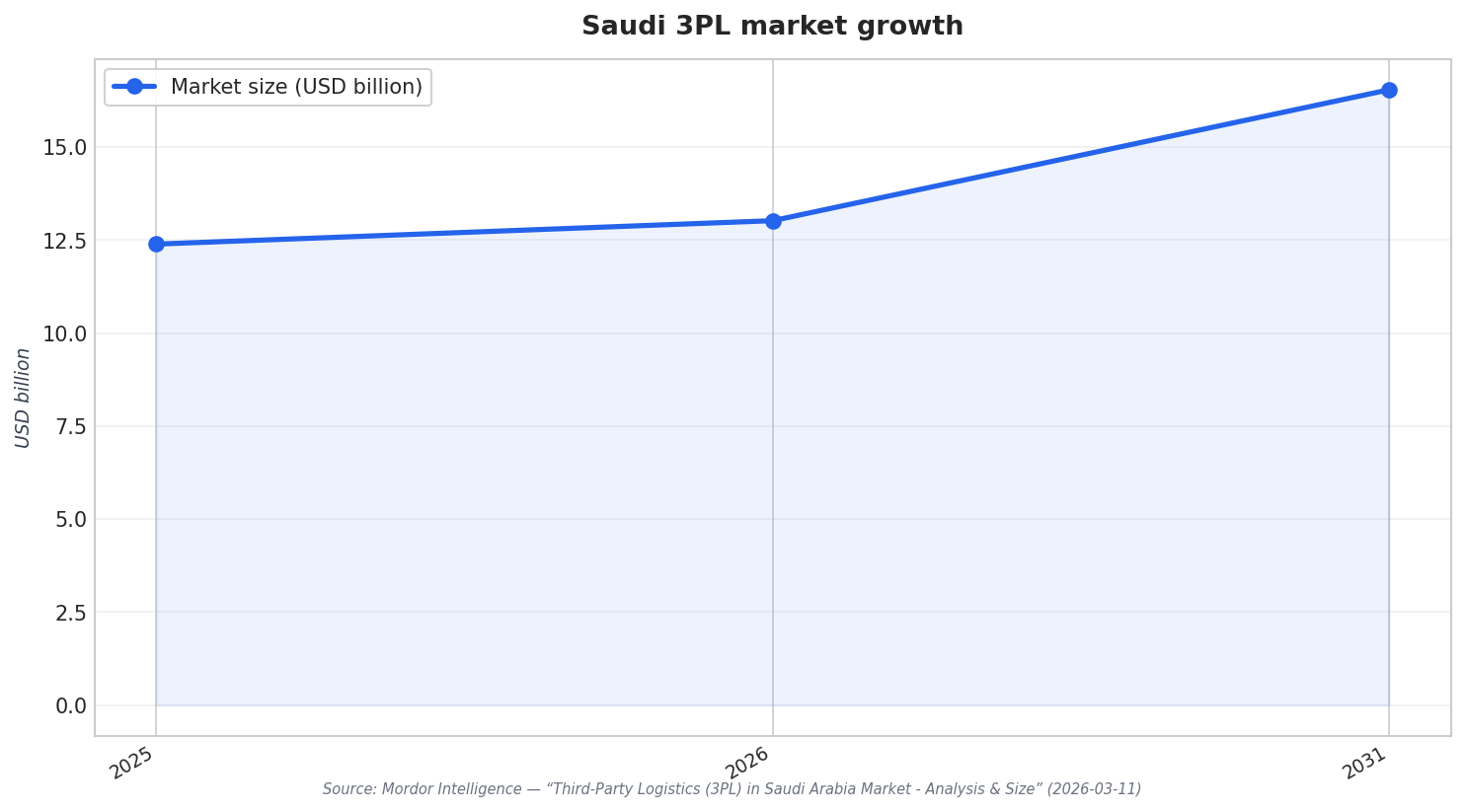

That demand is backed by the size and trajectory of the Saudi 3PL market. Mordor Intelligence values the Saudi Arabia third-party logistics (3PL) market at USD 12.39 billion in 2025 and estimates it will grow from USD 13.02 billion in 2026 to USD 16.54 billion by 2031, at a CAGR of 4.91% for 2026–2031. Within that mix, domestic transportation management led with a 43.33% share in 2025, while international transportation management is forecast to record a 5.2% CAGR through 2031. Those splits help explain why a combined domestic-plus-global platform can be positioned as a single “integrated” offer rather than a bundle of separate subcontracted services.

Why Consolidation Pressure Is Building in Saudi Logistics

Consolidation signals also show up in how analysts describe the competitive landscape and operating economics. A Mordor Intelligence freight and logistics outlook notes the market remains fragmented and that partnership-driven consolidation “quickened in 2024” as CEVA and Almajdouie merged networks to deliver integrated solutions from port handling to last-mile. It adds that operators able to capitalize on Vision 2030 PPP opportunities while embedding advanced analytics and sustainable assets will consolidate their share, while late adopters risk being pushed into subcontract status within orchestrated 4PL networks. The same outlook points to cost strain in e-commerce delivery: per-package cost outside the Riyadh–Jeddah–Dammam triangle runs 15–20% above GCC averages, driven by longer routes and sparse drop density—an operating reality that makes shared-network scale more valuable.

Vision 2030-linked infrastructure and contracting patterns reinforce the shift toward larger, integrated providers. In contract logistics, Mordor Intelligence values the Saudi Arabia contract logistics market at USD 1.23 billion in 2025 and estimates growth from USD 1.27 billion in 2026 to USD 1.51 billion by 2031, at a 3.52% CAGR. Transportation captured 64.30% share in 2025, but value-added services are forecast to grow at a 3.05% CAGR through 2031, indicating that differentiation increasingly comes from more than just trucking. Long-duration agreements matter too: contracts longer than three years held a 55.40% share in 2025 and are projected to expand at a 3.72% CAGR to 2031, which favors providers that can commit assets, systems, and service breadth across multiple years.

Finally, the deal’s timing fits a broader Middle East consolidation backdrop and a tightening “capability bar” inside Saudi Arabia. Mordor Intelligence sizes the Middle East 3PL market at USD 92.54 billion in 2026, growing at a 5.62% CAGR to reach USD 121.60 billion by 2031, and it highlights multiple investment and acquisition moves across the region. Inside Saudi Arabia, sustainability and compliance requirements are becoming procurement factors. Mordor Intelligence describes a 2025 SASO rule on carbon disclosure as embedding emissions transparency into tender criteria, and notes that providers investing in solar rooftops, electric fleets, and carbon-tracking platforms can command 8–12% pricing premiums. In this context, a CEVA–Almajdouie joint venture reads as more than a one-off partnership: it is a visible response to a market rewarding scale, integration, and audit-ready operations.

What happened in the CEVA–Almajdouie Saudi logistics merger deal?

How large is Saudi Arabia’s 3PL market, and what is the growth outlook?

Which 3PL service areas are most important in Saudi Arabia today?

What does the data say about long-term contracting in Saudi contract logistics?

What operating pressures are pushing Saudi logistics providers toward consolidation?

Talk to us for your needs in:

- Identifying Suitable Warehouse Sites in Saudi Arabia

- Customized Logistics and Supply Chain Analytics

- Logistics Network Design and Optimization

- Green Supply Chain and Sustainable Logistics Solutions

- Supply Chain Risk Management and Compliance

- Advanced Supply Chain Resilience and Agility

- Logistics Market Research and Strategic Analysis

- In-Depth Market Survey for Logistics

- Market Intelligence and Insights in Logistics

- Feasibility Study and Assessment in Logistics

- Integrated Warehousing Management Solutions

- Smart Warehousing and Automation Systems

- Sustainable and Green Warehousing Practices

- Port and Airport Logistics Optimization

- Digital Logistics Solutions

- Saudi Logistics Benchmarking