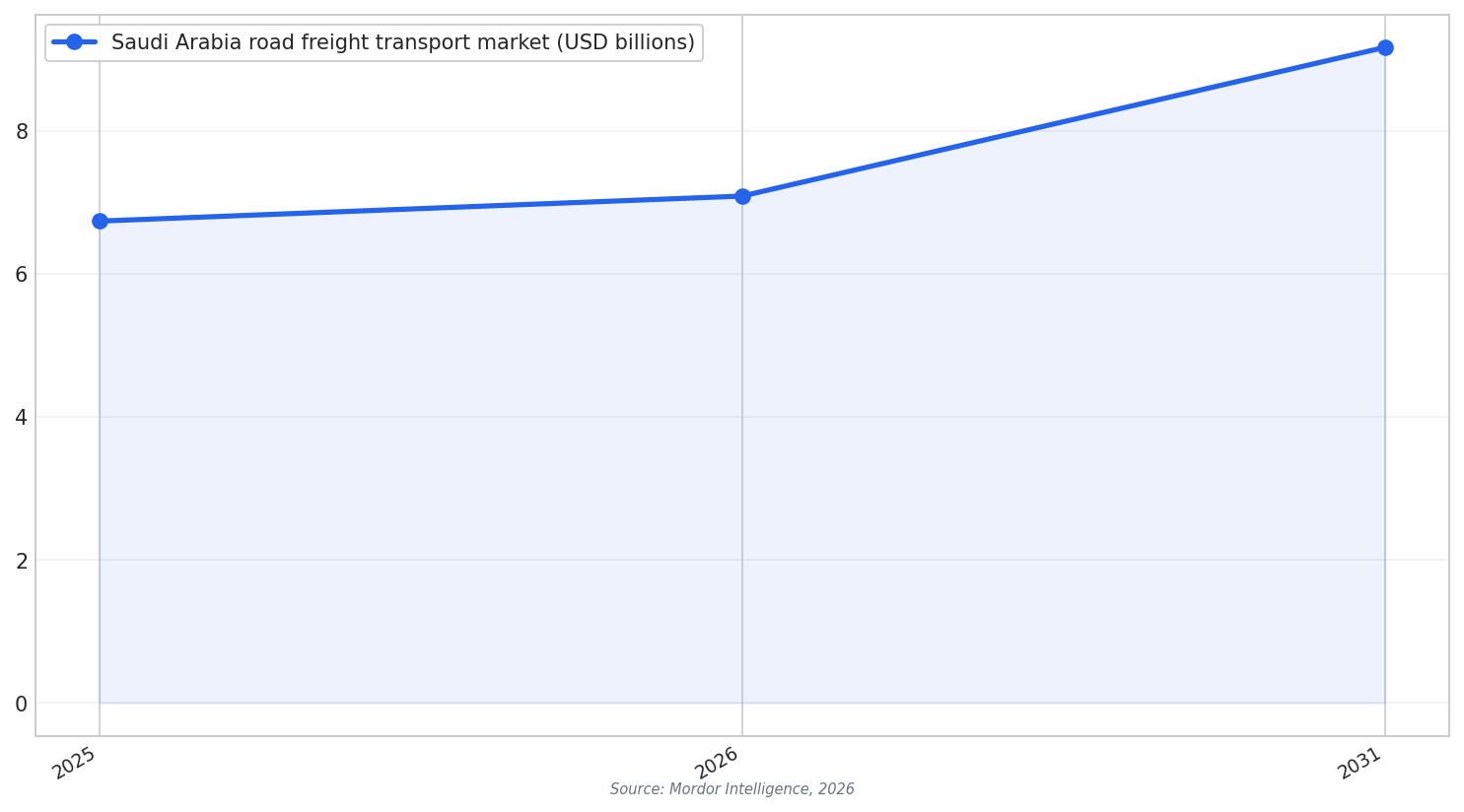

Saudi Arabia’s freight market is changing fast. Mordor Intelligence expects the Saudi Arabia road freight transport market to grow from USD 6.74 billion in 2025 to USD 7.09 billion in 2026, then reach USD 9.17 billion by 2031. As volumes rise, operators also face higher operating pressure from issues like driver shortages and congestion on the Riyadh-Dammam-Jeddah triangle. These forces are pushing fleets to look for new tools that improve efficiency and reduce wasted miles.

This freight demand is not just local. Domestic movements made up 61.25% of the road freight market in 2025, but international routes are set to grow faster at a 5.96% CAGR between 2026 and 2031. Long-haul is also dominant, with a 71.66% share in 2025, supported by a 73,000 km highway grid. These patterns matter because electric truck adoption is easier when routes, depots, and charging plans are predictable.

Several policy and investment signals support the next step in adoption. In 2023, the Saudi government implemented the “Green Fleet Initiative” under the National Transport and Logistics Strategy, issued by the Ministry of Transport and Logistics Services. Saudi Arabia has also allocated USD 1.5 billion for electric vehicle infrastructure development. Together, these steps reduce the risk of early deployments and help turn pilot fleets into repeatable operating models.

Why The Shift Is Moving Beyond Trials

The heavy-duty truck market shows why the Saudi electric truck fleet rollout is starting with targeted use cases. Mordor Intelligence values the Saudi heavy duty truck market at USD 8.76 billion in 2025 and forecasts USD 13.74 billion by 2030. Diesel still dominates. Internal combustion engines held 91.87% share in 2024. But the electric segment is forecast to expand at a 13.26% CAGR between 2025 and 2030, which signals growing interest even before full mass adoption.

Construction and mining are key demand engines. They held 43.28% of heavy-duty truck market share in 2024. At the same time, freight and logistics is the fastest-growing application, forecast at a 9.28% CAGR through 2030. This mix suggests a two-track rollout. High-utilization logistics corridors can support repeatable charging patterns, while large projects can adopt low-emission trucks inside controlled sites and captive routes.

Fleet economics and operating design also matter. Mordor notes that centralized overnight charging can reduce exposure to peak tariffs and streamline warranty management, and that kilometer accumulation helps reach parity faster versus subsidized gasoline. Hydrogen truck pilots are also mentioned as a way to address payload losses from lithium-ion batteries, but public hydrogen stations remain absent, so deployments stay limited to captive fleets. For many operators, this keeps the near-term focus on controlled electric pilots that can scale as infrastructure and planning improve.

What is driving the Saudi electric truck fleet rollout right now?

How fast is the freight market growing in Saudi Arabia?

Are electric heavy-duty trucks already mainstream in Saudi Arabia?

Which freight patterns matter most for fleet electrification planning?

Talk to us for your needs in:

- Identifying Suitable Warehouse Sites in Saudi Arabia

- Customized Logistics and Supply Chain Analytics

- Logistics Network Design and Optimization

- Green Supply Chain and Sustainable Logistics Solutions

- Supply Chain Risk Management and Compliance

- Advanced Supply Chain Resilience and Agility

- Logistics Market Research and Strategic Analysis

- In-Depth Market Survey for Logistics

- Market Intelligence and Insights in Logistics

- Feasibility Study and Assessment in Logistics

- Integrated Warehousing Management Solutions

- Smart Warehousing and Automation Systems

- Sustainable and Green Warehousing Practices

- Port and Airport Logistics Optimization

- Digital Logistics Solutions

- Saudi Logistics Benchmarking